If you've recently searched for car insurance quotes - or had a nasty surprise at renewal time - you're probably wondering what everyone else is paying. The honest answer? It depends. Car insurance is one of those costs that varies wildly from person to person, and two drivers living on the same street can end up paying very different premiums.

That said, it's useful to have a rough benchmark. In this guide, we'll walk through what UK drivers can realistically expect to pay in 2026, what drives those costs up (or down), and how to make sure you're not overpaying. No scare tactics, no hard sells - just practical information.

What Does Car Insurance Typically Cost in 2026?

Before we get into numbers, a quick caveat: there's no single "average" that applies to everyone. The figures below are based on industry trends, insurer data, and market analysis from organisations such as the Association of British Insurers — they’re ballpark ranges, not guarantees.

, and market analysis - they're ballpark ranges, not guarantees.

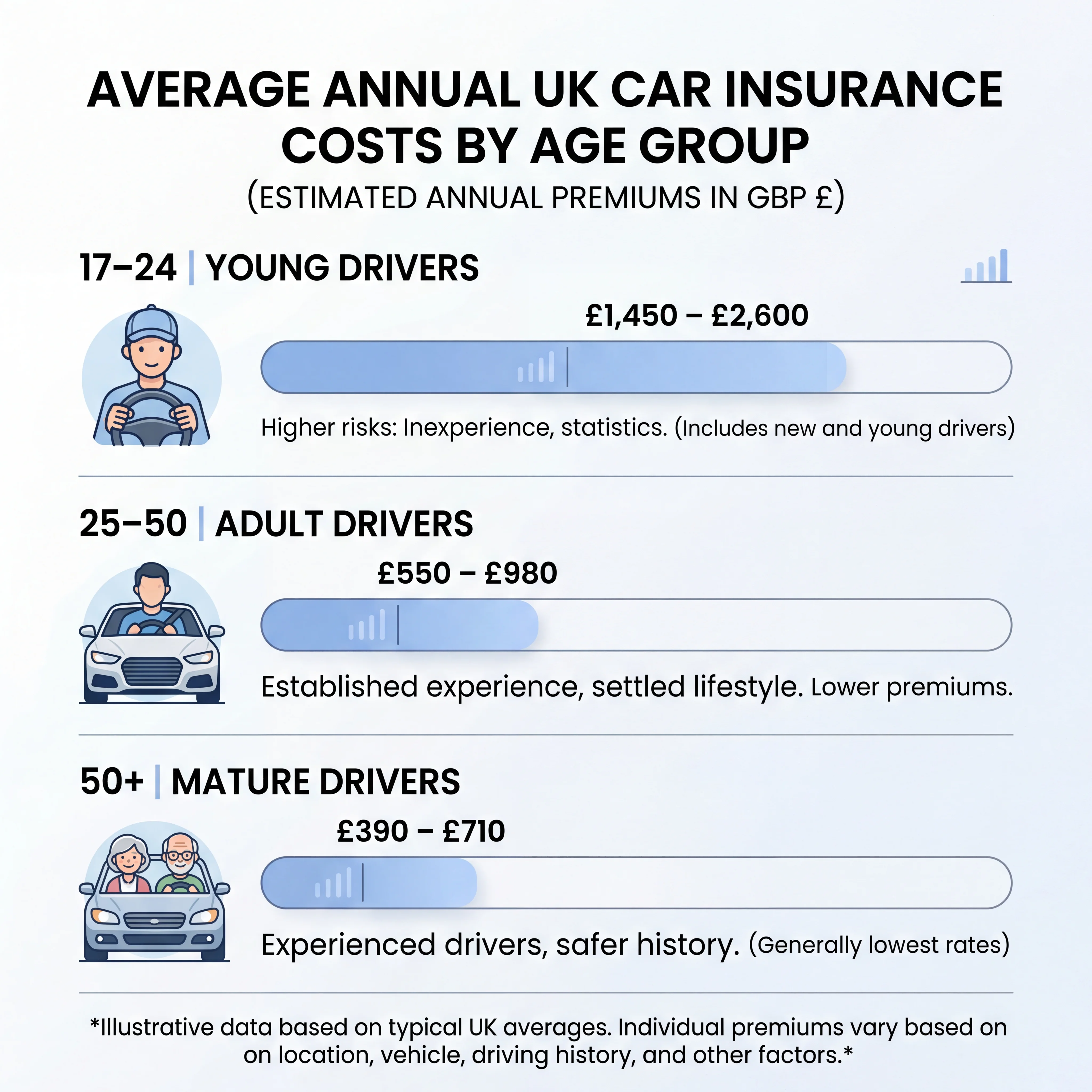

Young Drivers (17–24)

This is the age group that feels the pain most. If you're a young or newly qualified driver, expect annual premiums somewhere in the region of £1,400 to £2,800, depending on your car, location, and whether you've built up any no-claims bonus yet. Some younger drivers in high-risk areas or with powerful cars could see quotes well above £3,000.

Adults (25–50)

Once you're past 25, things start to calm down. Most drivers in this age range pay somewhere between £500 and £1,100 a year. If you've got a clean record, a sensible car, and a few years of no-claims discount behind you, you'll likely be towards the lower end.

Older Drivers (50+)

Experienced drivers with long claims-free histories often enjoy some of the lowest premiums, typically in the range of £350 to £700. However, premiums can begin creeping up again once you reach your mid-70s, as insurers start factoring in higher accident risk.

These ranges aren't set in stone, and your own quote could fall outside them. The point is to give you a rough idea of where things stand - not to promise you a specific price.

What Affects the Cost of Car Insurance?

Insurers weigh up dozens of factors when calculating your premium. Here are the ones that make the biggest difference:

Your age is the single most influential factor. Younger drivers are statistically more likely to be involved in accidents, and that risk is baked into the price. There's not much you can do about this one other than wait it out - premiums drop significantly once you hit your mid-twenties.

Where you live matters more than most people realise. Your postcode tells insurers a lot about the likelihood of theft, vandalism, and accidents in your area. Urban postcodes - particularly in parts of London, Birmingham, and Manchester - tend to attract higher premiums than rural ones.

The car you drive plays a big role too. Every car is assigned an insurance group from 1 to 50, based on things like engine size, repair costs, safety features, and how attractive it is to thieves. A small hatchback in group 5 will cost significantly less to insure than a sports car in group 35.

Your driving history is another key factor. Any claims, convictions, or penalty points on your record will push your premium up. Conversely, a clean driving history and a healthy no-claims bonus can knock a serious chunk off your annual cost.

Annual mileage also comes into play. The more you drive, the more exposure you have to potential accidents. If you're only doing 5,000 miles a year, that works in your favour. Just don't be tempted to understate your mileage - if you need to make a claim and your insurer finds out you've been driving more than you declared, it could void your policy.

The level of cover you choose affects the price, though perhaps not in the way you'd expect. Comprehensive cover is often cheaper than third-party only, partly because insurers associate third-party-only policies with higher-risk drivers. Car insurance is also a legal requirement in the UK, as outlined by GOV.UK, which is why at least third-party cover is mandatory for drivers on public roads. More on that in the FAQ below.

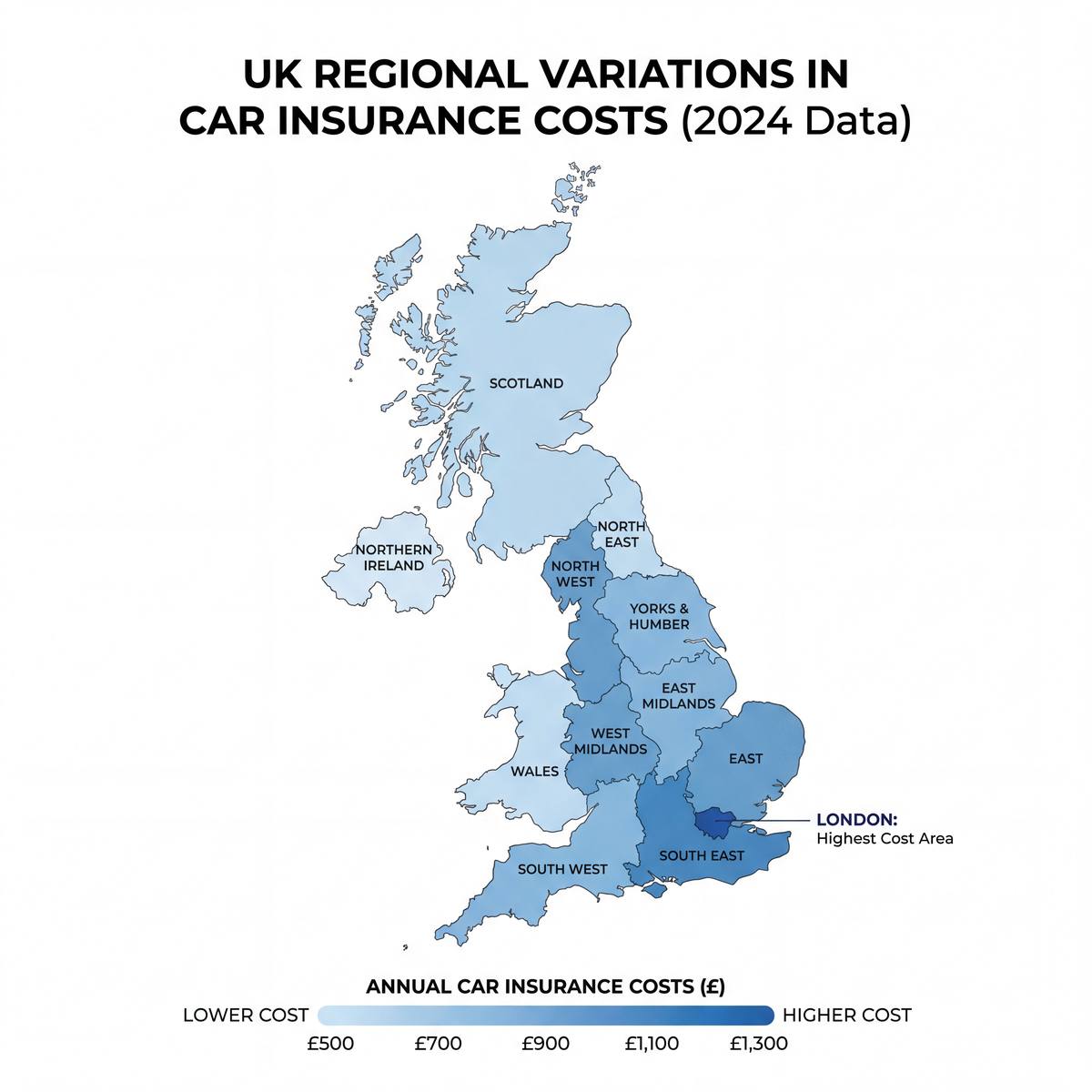

Car Insurance Costs by Location

Where you park your car overnight can make a surprising difference to what you pay.

London is consistently the most expensive area for car insurance in the UK. Higher traffic density, more accidents, and greater theft risk all contribute. Drivers in some London boroughs can pay 30–50% more than the national average for equivalent cover.

Other major cities like Birmingham, Manchester, and Leeds also tend to have above-average premiums, largely for the same reasons - more cars on the road means more claims.

By contrast, drivers in rural parts of Scotland, Wales, and the South West of England often enjoy some of the lowest premiums in the country. Fewer cars, fewer claims, fewer thefts - it all adds up to cheaper insurance.

If you're on the border between two postcode areas, it's worth noting that even a short move can sometimes affect your premium. It's not something to base a house move on, obviously, but it's useful to know.

Cost by Driver Type

Not all drivers fit neatly into age brackets. Here's how some common driver profiles tend to fare:

New drivers face the steepest premiums regardless of age. If you've just passed your test at 30, you'll pay more than a 30-year-old with ten years' experience. Building up a no-claims bonus is the fastest way to bring costs down.

High-risk drivers - those with previous claims, convictions, or certain medical conditions - will typically pay more. Specialist insurers exist for drivers with non-standard histories, and they're sometimes more competitive than mainstream providers, so it's worth looking beyond the big names.

Low-mileage drivers can often save by choosing a policy that reflects their actual usage. Some insurers offer pay-per-mile or low-mileage discounts. If you mainly use your car for short local trips, it's worth flagging this when you get quotes.

Multi-car households may benefit from multi-car policies, where insuring two or more vehicles with the same provider can unlock a discount. It's not always cheaper - sometimes separate policies still win - but it's an option worth checking.

How to Reduce Your Car Insurance Premium

There's plenty of generic advice floating around, so let's focus on the things that actually make a meaningful difference:

Shop around every single year. This is the biggest one. Loyalty rarely pays in insurance. Your renewal quote is almost never the most competitive deal available, and switching could save you hundreds of pounds. Set a reminder a few weeks before your renewal date.

Increase your voluntary excess - but only to a level you could genuinely afford to pay if you needed to claim. Bumping it up from £250 to £500 can noticeably reduce your premium, but setting it at £1,000 when you don't have that kind of cash sitting around is a false economy.

Consider a black box (telematics) policy, especially if you're a young or new driver. These policies monitor your driving habits and reward safe driving with lower premiums. They're not for everyone, but they can cut costs substantially if you're a careful driver who mostly drives during the day.

Build and protect your no-claims bonus. This is genuinely valuable. A full no-claims discount of five or more years can reduce your premium by up to 70% with some insurers. Some providers also offer no-claims protection - it costs a little extra, but it means a single claim won't wipe out years of discount.

Pay annually if you can afford to. Monthly instalments typically come with interest, adding 15–30% to the total cost. Paying upfront saves real money over the course of a year.

Don't over- or under-estimate your mileage. Be accurate. Overestimating means you're paying for cover you don't need. Underestimating could cause problems at claim time.

Think carefully about modifications. Even cosmetic changes like alloy wheels or tinted windows can increase your premium. Performance modifications almost certainly will.

Why Comparing Quotes Matters

Here's something that catches a lot of people off guard: two insurers can look at the exact same driver profile and come back with wildly different prices. One might quote £600 while another quotes £900 for identical cover. That's not a mistake - it's because every insurer uses its own pricing model and risk appetite.

This pricing variation is widely discussed by consumer finance platforms like MoneySavingExpert, which regularly highlight the importance of comparing quotes rather than relying on a single provider.

This is why comparison is so important. It's not about finding a magic loophole or gaming the system. It's simply that the most competitive insurer for your neighbour might not be the most competitive one for you. The only way to find out is to compare.

Comparison websites are a good starting point - for example, you could compare quotes from 120+ UK car insurance providers and you could save up to £518*. Not every provider appears on comparison sites though. Some - like Direct Line and Aviva - don't, so it's worth checking a few of those directly as well.

Also, don't just look at price. Check what's actually included: courtesy car, legal cover, breakdown assistance, windscreen cover. A slightly more expensive policy that includes these extras might work out better value than a bare-bones one where you'd need to add them separately.

Wrapping Up

The cost of car insurance in the UK is a moving target. It depends on who you are, what you drive, where you live, and how you drive. There's no shortcut to finding the right policy at the right price - but comparing quotes regularly and understanding what drives your premium puts you in a much stronger position.

If your renewal is coming up, don't just accept it. Spend 20 minutes comparing, and you might be surprised at what you could save.

*51% of consumers could save £518.14 on their Car Insurance. The saving was calculated by comparing the cheapest price found with the average of the next four cheapest prices quoted by insurance providers on Seopa Ltd's insurance comparison website. This is based on representative cost savings from June 2025 data. The savings you could achieve are dependent on your individual circumstances and how you selected your current insurance supplier.

Frequently Asked Questions

Why is car insurance so expensive for young drivers?

It comes down to risk. Statistically, drivers aged 17–24 are significantly more likely to be involved in accidents - particularly serious ones. Insurers price that risk into premiums. It feels unfair if you're a careful young driver, but it's based on data from millions of policies. A telematics policy can help prove you're a safe driver and bring costs down more quickly.

Is comprehensive cover really cheaper than third-party only?

It can be, yes. This sounds counterintuitive, but many insurers view drivers who choose third-party-only cover as higher risk - the assumption being they may be cutting corners on cost. As a result, third-party policies sometimes come back more expensive than comprehensive ones. It's always worth getting quotes for both and comparing.

Does my job title affect my car insurance?

Surprisingly, yes. Insurers use your occupation as part of their risk assessment. Certain job titles are associated with lower claim rates, and the way you describe your role can make a small but real difference. For example, "chef" and "kitchen worker" might return different quotes even if the job is essentially the same. Be honest, but if your role could be described in more than one way, try both and see.

How often should I compare car insurance quotes?

At minimum, once a year before your renewal date. Ideally, start looking around three to four weeks before your policy expires - this tends to be the sweet spot for competitive pricing. Some people also check mid-term to see if the market has shifted significantly, though switching mid-policy can involve cancellation fees.

What's the most cost-effective way to get car insurance?

There's no single answer, but the combination that tends to produce the lowest premiums is: a small, low-group car; a clean driving record with a full no-claims bonus; annual payment; a reasonable voluntary excess; and - crucially - comparing quotes from multiple providers every year. If you're a young or new driver, a telematics policy is often the most cost-effective route.

Can I insure a car I don't own?

Yes. You don't have to be the registered keeper to insure a vehicle. However, the policyholder must be the main driver. A common mistake is putting a parent as the main driver on a young person's car to get cheaper insurance - this is called "fronting" and it's fraud. If you're caught, your policy will be cancelled and you could face prosecution.